Supply AND Demand

Successful industrial policy requires both

Welcome to Charged States, a publication focused on the geopolitics of the energy transition. The goal is to help explain politics to the energy world, energy to the political world, and a little bit of both to everyone else.

Earlier this month, the Department of Energy took a 5% equity stake in Lithium Americas and a 5% stake in their Thacker Pass lithium project joint venture (the DOE had originally finalized a loan for the project last year). Last week, the Administration announced an equity stake in Trilogy Metals to support development in Alaska. And reports suggest that the Administration will continue to utilize equity stakes to support projects domestically and abroad.

In the DOE’s announcement on Thacker Pass, Energy Secretary Wright says “Thanks to President Trump’s bold leadership, American lithium production is going to skyrocket.”

This is not a post about their equity strategy, that will be for another day.

On the same day of the Thacker Pass announcement, the $7,500 IRA EV Tax credit officially expired. The “30D” tax credit became public enemy number one for Republicans attacking the Biden Administration’s green industrial policy and it was eliminated in this summer’s OBBB. The Trump Administration also aims to lower emission standards that would drive demand for EVs. The leading driver of demand for lithium is batteries for EVs.

Ford CEO Jim Farley said these policies could see EV sales fall by half in the U.S. and the domestic market will be “way smaller than we thought.” We should expect poor domestic EV sales over the next few quarters as demand drops and the automakers wade through this transition. GM’s CFO said “EV demand is going to drop off pretty precipitously.” For comparison, EV sales in Germany dropped by 27% in 2024 following the elimination of similar subsidies.

Focusing on supply while cutting demand will only leave us in the same spot we are now - reliant on foreign supply for key parts of the supply chain.

Unlocking supply

In many ways the Trump Administration listened to what every mining company or expert said was necessary during policy roundtables during the Biden Administration to unlock supply and they are now pushing those policies.

The Administration’s industrial policy towards critical minerals should not be that surprising, as it follows the major themes of the Republican Party and Trump agenda.

Cutting administrative hurdles that block natural resource production - “Drill, Baby, Drill” was official GOP policy long before Sarah Palin said it on a debate stage in 2008

Focus on defense over climate - this is the Republican Party

Anti-China

Art of the Deals - dealmaking process is new but this is the supposed “dealmaker in chief.”

Tariffs - the President’s favorite word

Strong domestic focus (aka MAGA) - there is talk of international deals but from my experience, the focus will be on domestic projects

If there is a coherent policy, then it is a supply-side approach to use administrative interventions, creative financing, and trade policy to support new sources of domestic production.

The stated goal of the equity stake in Thacker Pass is to unlock a domestic supply of lithium (once again, we can debate on the merits of the policy) by supporting lithium carbonate production (both mining and processing) at the Nevada mine. The project was progressing nicely before the Administration’s actions and is important for domestic production. Lithium carbonate is a processed lithium chemical used directly in LFP batteries or as a precursor for lithium hydroxide, which feeds nickel-based lithium-ion chemistries

Increasing production of critical minerals was included in the “Unleashing American Energy” EO with the aim of “Restoring America’s Mineral Dominance.” They have followed this with subsequent ones, including on deep sea mining. Section 232 investigations into copper and processed critical minerals also aim to support domestic production.

The Department of the Interior has added a few projects to the FAST-41 permitting process and more mining projects to the FAST-41 Transparency Projects to increase transparency in the permitting process. (Important to note that this is not the FAST-41 process and does not guarantee faster permitting)

Increased funding for domestic production is a key mechanism to increase supply. Their equity stake/price floor for MP Materials supports both domestic production at Mountain Pass and domestic permanent magnet production.

The OBBB provided over $7 billion to the DoD to fund critical minerals. Launched by the Biden Administration and not even 3 years old, the Office of Strategic Capital is now the one of the most important tools for critical minerals in the USG. Additionally, the DOE announced the availability of nearly $1 billion for funding for critical minerals projects from remaining BIL funding.

And we should expect more initiatives to support the supply-side - permitting reform remains a priority but requires bipartisan support to pass the Senate. And we are awaiting Commerce’s 232 findings.

These initiatives are long overdue. Permitting is too slow in the United States. Funding - especially creative mechanisms - are necessary to either crowd in private financing or build supply chains they will not invest in. And tariffs can play a role in building a new supply chain. Our current dependency requires a whole-of-government approach and willingness to take on financial risks. Yet as the debate over critical minerals intensifies, one essential piece of the equation continues to be overlooked: demand.

Demand is key

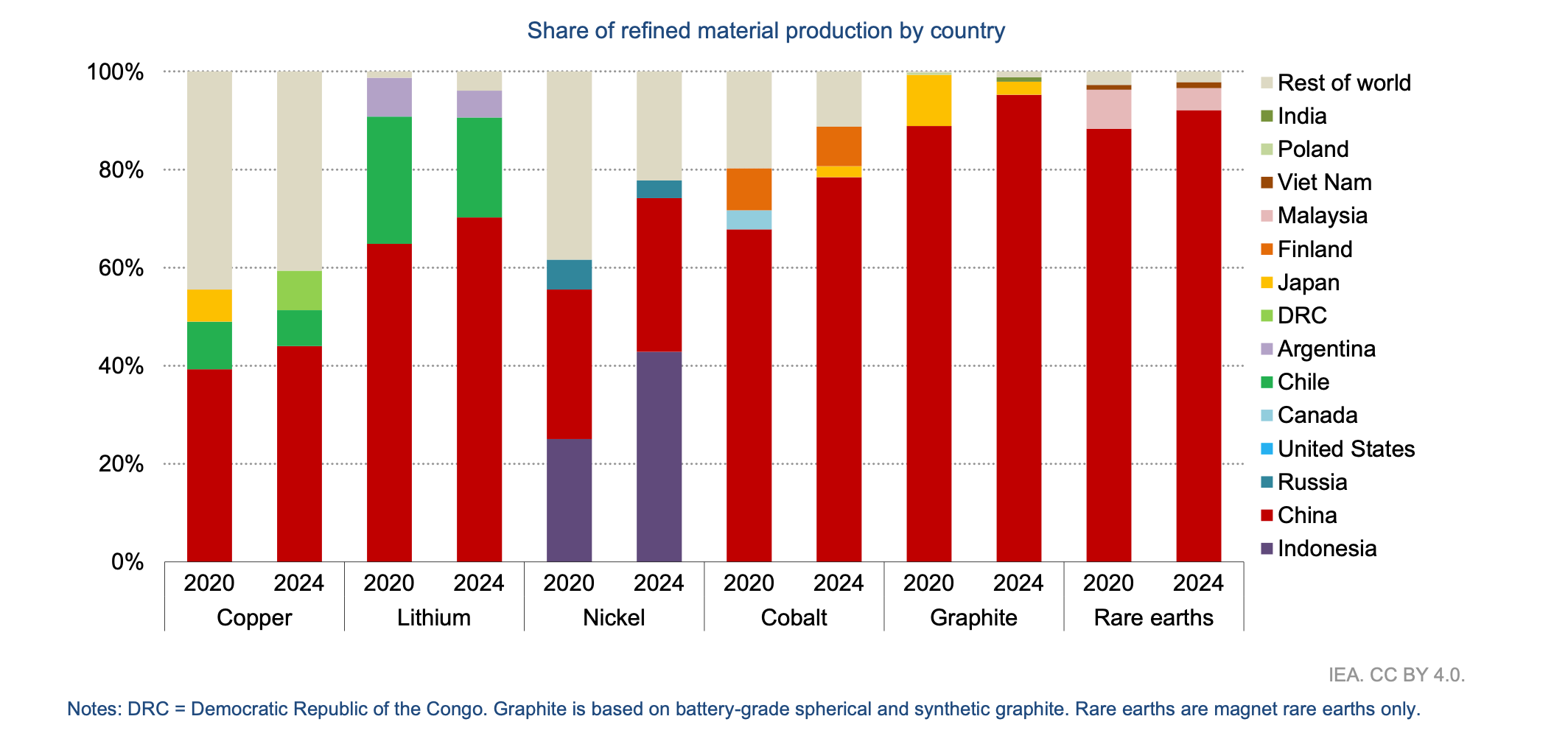

If you discuss critical minerals in Washington, a variation of this chart from the IEA will be shown.

The chart quickly illustrates the chokehold China has in the supply chain. China (in the red on the chart) dominates refining of critical minerals. The U.S. is barely visible. The graph is a quick, easy way to communicate the issue at hand.

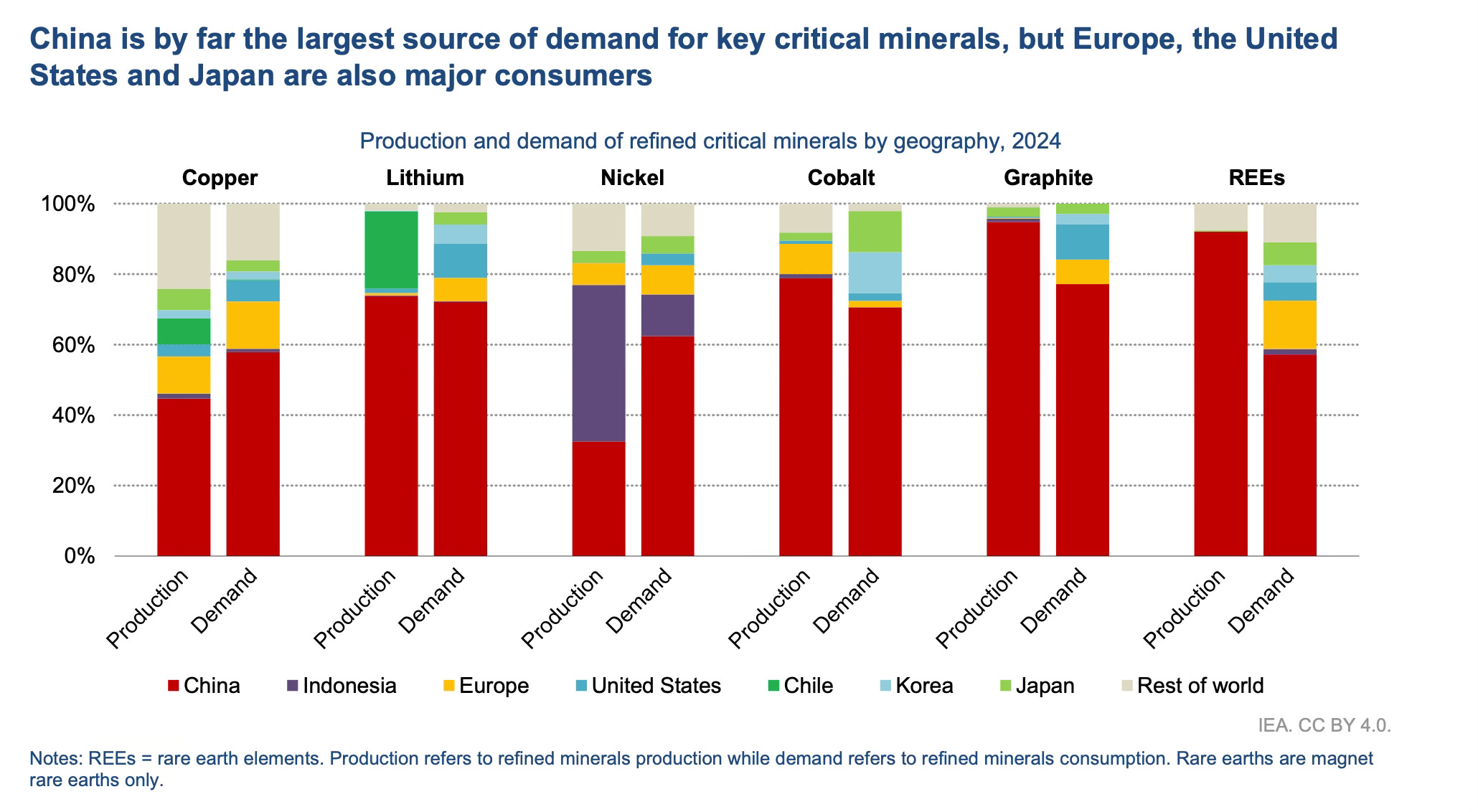

But the chart below tells a more complete story. China is the key node in the supply chain because they are the demand drivers for these commodities.

The immediate criticism of this chart is that China is the main demand driver because they export technologies to the world. That is true, but incomplete.

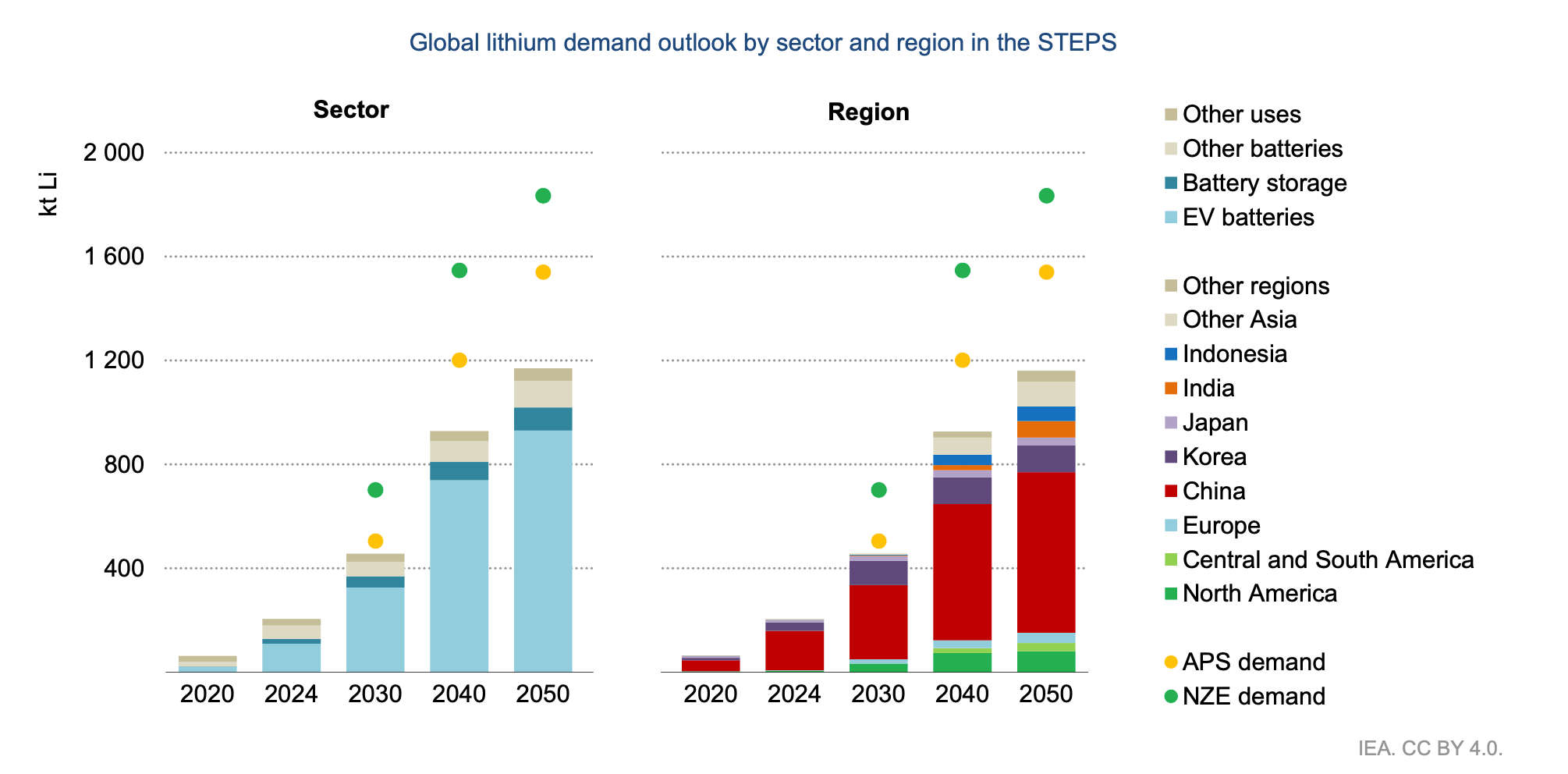

Let’s look specifically at lithium because of Thacker Pass.

As shown in the graph below, battery storage - for both EVs and Battery Energy Storage Systems (BESS) - are the main demand drivers for lithium.

And China is the global leader in both EVs and BESS deployment. These numbers represent batteries for vehicles or BESS sold domestically, not for export.

China’s demand continues to grow in both sectors. Chinese EV sales grew 44% y-o-y in the first 6 months of 2025. They have nearly 80GW battery storage and now aim to grow to 180GW by 2027.

It is this enormous domestic demand that underpins China’s dominance across critical mineral supply chains. A large and predictable domestic market enables Chinese companies to invest confidently in overseas mining projects, knowing they can rely on a stable customer base at home.

This demand also sustains investment in midstream processing, precursor, and cathode manufacturing, creating economies of scale that reinforce China’s market position. As battery and EV manufacturing expands, they anchor an integrated and resilient supply chain network.

By contrast, the United States will not be able to onshore its supply chains without developing a globally competitive domestic market that provides scale, certainty, and investment signals.

Real World Example

How does strong Chinese demand and waning American demand impact current projects?

Last week, Liontown Resources announced that Ford will delay their lithium offtake agreement for the Kathleen Valley project in Australia. Liontown pushed hard to be a Western-focused lithium project through agreements with Tesla, Ford, & LG. Ford has pushed off their agreement due to slowing EV demand and will not take lithium from Liontown in 2027 and 2028. The end result? The Australian miner will have to sell lithium earmarked for an American automaker to China. Liontown did everything they could to be a Western-focused miner but are left having to sell to China because of weak demand.

The missing middle

Thacker Pass will produce lithium carbonate, used in LFP cathodes or processed into lithium hydroxide. LFP is the preferred battery chemistry for both affordable EVs and BESS due to their lower cost and longer cycle life (meaning they can be charged and discharged more times than other chemistries). But China controls over 98% of production. Lithium hydroxide is used in nickel-based lithium-ion batteries, the most popular choice for U.S. automakers due to their longer driving ranges. And for nickel-based lithium-ion batteries (unlike LFPs), the market is not completely dominated by Chinese companies.

Right now, the United States does not have commercial scale lithium hydroxide production1, nor precursor cathode active material production, or cathode production. Without that midstream, lithium from Thacker Pass will be exported before it ever reaches a U.S. battery line.

So what does this have to do with demand? These processing facilities are highly capital-intensive and operate on thin margins, especially in the United States. To remain viable, they must run at high utilization rates to spread fixed costs and maximize revenue. This requires a stable base of guaranteed customers and predictable demand. Projects will struggle to attract investment or sustain operations without the requisite sustained demand.

The current Trump Administration approach feels like a copy-paste of their traditional oil and gas policy: out of the ground and into the market. But the U.S. already has significant demand and midstream infrastructure for fossil fuels. Unless demand grows enough to justify processing and manufacturing investment, we will spend the next few years discussing at policy roundtables how the U.S. needs to support demand-side initiatives to make critical minerals projects investable.

If we want to build a full, secure supply chain, the U.S. needs to combine the Trump Administration’s strategy on unlocking supply with incentives that drive demand…like the policies they just eliminated.

Tesla is ramping up production of lithium hydroxide refinery in Texas but info is limited and the facility will only produce for Tesla.